An old Booklet A opened by your parents and forgotten for years. An abandoned employee savings plan from a previous job. An old account abandoned by your elderly parents. Or even life insurance, a PER or even a PEL which you can inherit without knowing it. A little-known system allows you to get your hands on these forgotten assets: Ciclade.

“My father opened a PEL in my name in the 70s or 80s. How can I know the amount? And how can I get it back? » This question asked by Franck in 2023 calls for a simple answer: go to Ciclade.fr !

Never heard of this official site linked to the Caisse des Dépôts? Damage. Not surprising either since, apart from very rare news on “ Bercy info ” And impots.gouv.fror the annual zoom on the statistics of savings forgotten in the media, Ciclade rarely occupies the forefront of the media scene…

Even if the spotlight on annual statistics sometimes has surprising repercussions: in 2023, no less than 11 million searches for forgotten treasures have been carried out! For 15.1 million since the portal opened in 2017. Last year, these millions of searches resulted in 223,774 matches… and therefore as many requests for restitution of forgotten savings. The reward ? 747 euros recovered on average, per beneficiary, in 2023, for an average peaking at 1,784 euros since 2017.

But there still remains 7 billion euros waiting to be claimed ! However, due to lack of demand, after around twenty years of sleeping at the Caisse des Dépôts, these forgotten savings are automatically returned to the State. Definitely. How to recover the money before the deadline? Manual.

If you have forgotten an old booklet or an employee savings plan…

Meeting on ciclade.caissedesdepots.fr, this service being a mission of the Caisse des Dépôts. Follow the instructions or click directly on “ start my search “. First step: carry out a search in your name, therefore filling in your personal data (surname, first name, date of birth, nationality, etc.) without necessarily mentioning an account or contract number. Check. Confirm.

Heads up, failed, you land on the following screen…

On the head side, bingo, Ciclade tells you: “ There is a possible match to your search », without indicating at this stage whether it is a Livret A, another bank account, an old company savings plan or even life insurance whose expected maturity (1) has long been outdated. It is only in the event of a possible match that the Caisse des Dépôts offers to create a personal space on Ciclade. You will then be required to provide identification and proof of address.

Afterwards ? The editorial team was able to test the system from A to Z from 2017 but also more recently, during the summer of 2021. The process is almost unchanged and still just as simple in the case of an account belonging to you and which you had forgotten. Once your identity has been proven when creating your account, you must provide your bank details (RIB) in order to transfer the amount owed to you.

The last procedure carried out by the editorial staff resulted in a transfer in just 3 days! Follow-up on receipt of proof of payment by email, where the institution informs you of the need to declare these assets for taxes or not. On the bank account in question, the transfer appeared as coming from the Caisse des Dépôts with a wording specifying that the sum came from an inactive investment (a Livret A in this case).

If a deceased loved one left you life insurance or another investment…

It gets complicated when the product forgotten for many years is not in your name! Both for life insurance that you should have benefited from and for another savings product that you should have inherited…

Booklet, PEL, employee savings plan or inheritance current account. This is the weak point of Ciclade: all searches are carried out in the name of the holder of the account or contract concerned. Bank assets (excluding life insurance) include an inheritance in the event of death, so you must carry out a search in the name of your deceased loved ones (parents, grandparents, etc.) if you are one of their beneficiaries. For this request, bring with you the dates of birth and death of the deceased.

In the event of a match, Ciclade invites you to create a personal space in your name: an identity document is required. It is up to you to then provide a substantial list of supporting documents proving your rights: death certificate, inheritance documents, RIB, etc. Once these supporting documents have been sent, the Caisse des Dépôts must verify your rights to these assets (booklet, home savings plan, PEE, etc.), which sometimes requires the intervention of a notary.

The process remains free but it takes longer: “processing your request takes on average 90 days because it involves many players (banks, insurance companies, employee savings organizations, notaries, etc.),” explains Ciclade. “In addition, verifications and cross-checking of information on the amounts requested are necessary. »

Inheritance: how to share the estate without tearing each other apart

Life insurance. An even more delicate task… Life insurance is a “non-inheritance” product. The capital does not necessarily go to the beneficiaries of the inheritance but sometimes to other people listed as beneficiaries in the contract.

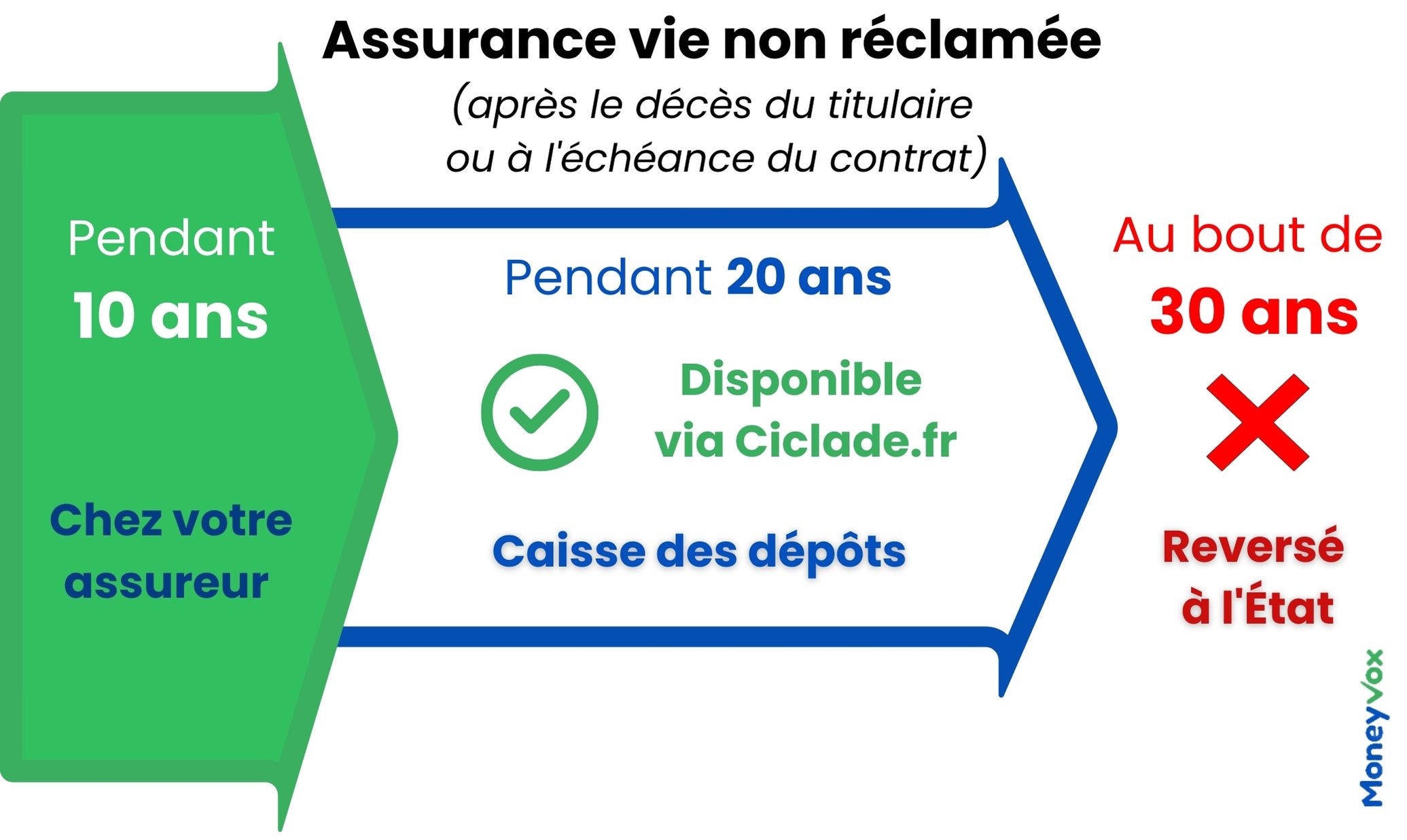

At death, when everything goes well, you do not have to claim to recover the capital of a life insurance policy of which you are the beneficiary: it is the insurer who must find the beneficiaries designated in the contract. Except… sometimes the insurer doesn’t succeed. Sometimes due to lack of zeal, sometimes because the beneficiary clause is imprecise, sometimes because he is unaware of the death, etc. The insurer then keeps the funds for a period of 10 years and is supposed to continue its research.

In the event of a “recent” death (less than 10 years old), you must make your request to the Agira association, which lists these claims for all insurers. Beyond 10 years, Ciclade takes control. The process is the same as that detailed above for other investments. But how do you know if you are a beneficiary?

If you are one of the compulsory heirs (children in particular), the money may come to you by default if the beneficiary clause is empty or filled out in a “standard” way (for example: “my spouse (…) is designated as beneficiary.” , failing that my children, (…) in equal shares between them, failing that my heirs).

Even if you are not one of the heirs, nothing prevents you from launching a request on Ciclade (using the death certificate and the civil status of the deceased): the process is free. If the request is positive, after verification, the funds will be returned.

If you forgot a retirement savings product…

Good news: the law of February 26, 2021 addressed the subject of forgotten retirement savings plans. This time it is not about the retirement contracts from which you are a beneficiary… but about the retirement savings plans that you opened yourself and whose existence you forgot at retirement age. Now the section “ My retirement savings » ofInfo-retraite.fr provides you with all the information you need to get your hands on contracts in your name. Here is the process… if you have just retired.

Retirement savings: instructions for finding your forgotten money

You are retired for more than 10 years ? Your contract will be considered escheated, since abandoned for a decade after expiry (the legal retirement age). New for 2023: old “retirement” contracts (Madelin, Perp, article 83, Perco, etc.) which have fallen into oblivion and are unclaimed after around ten years after this deadline (the legal age) are repatriated to the Deposit fund. And therefore available via Ciclade.fr for 20 years.

When are your savings (or those left to you) found on Ciclade?

On Ciclade, you will only find old accounts or contracts that have been inactive for so long that your bank or insurer had to transfer them to the Caisse des Dépôts, a public financial institution. When does an investment transfer to the coffers of the Caisse des Dépôts? In two step.

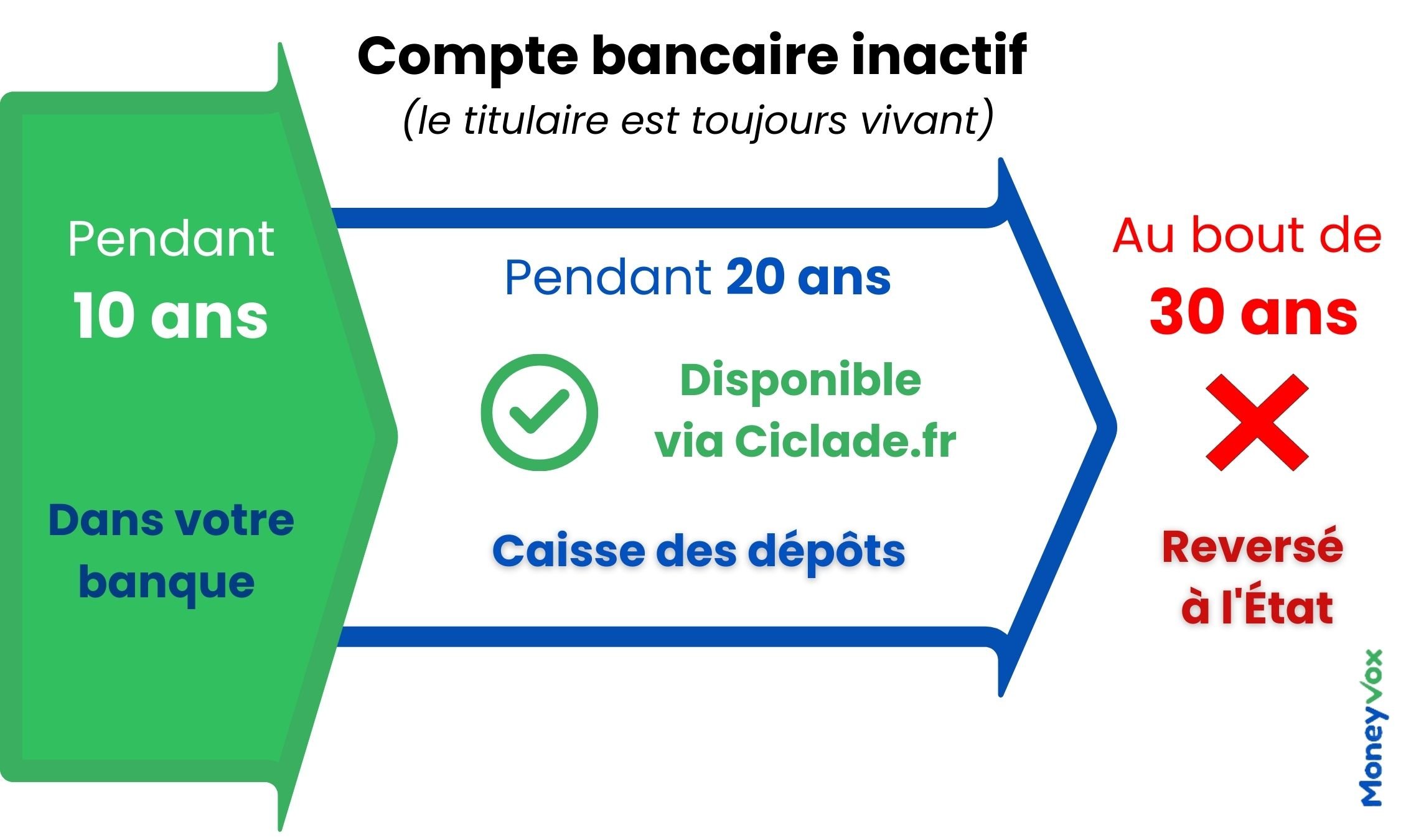

First stage : the account manager must designate him as inactive or unclaimed. For a Bank accountit is considered inactive after 1 year without any movement or sign of life from the holder. For a company savings plan (PEE)A savings account or one accounts titlesinactivity is activated after 5 years without signs of life.

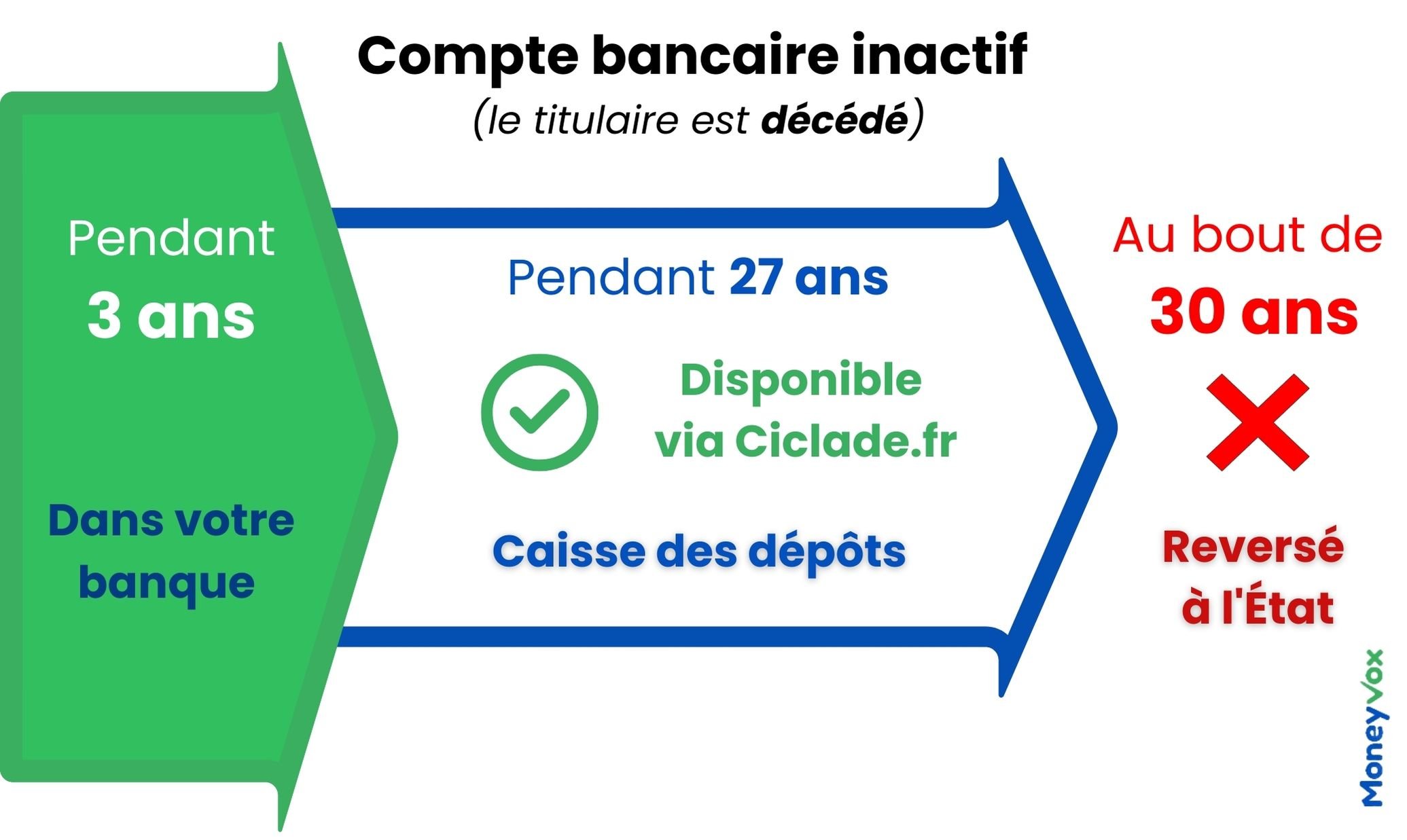

In case of deaththe account or investment is immediately considered unclaimed if the bank or insurer does not identify the beneficiaries (and they do not come forward).

Second step. An inactive or unclaimed account will remain at the bank for 3 or 10 years depending on the case before transferring to the Caisse des Dépôts.

Where is the forgotten money?

The ELP, an exception. The “orphan” home savings plan (with no sign of life of the holder who has no other account in the bank) is kept for 20 years by the bank… before being transferred to the Caisse des Dépôts. The unclaimed PEL is then available for 10 years on Ciclade before being returned to the State.

Also read, on Ciclade

(1) Life insurance with a fixed term, provided for in the contract. Beyond this deadline, the savings accumulated cease to produce interest.

(2) Source: annual public report of the Court of Auditors, February 2019.