This is one of the imperfections of withholding at source: credits and reductions are not taken into account in calculating the withholding rate! This is why the tax authorities pay you an advance in January. But, in certain cases, we must refuse the poisoned gift of mid-January 2024: here is why, and how to proceed.

Since 2019, in mid-January, the tax authorities have played Santa Claus again for nearly 9 million households. If you are used to benefiting from a tax reduction for donations to charities, for rental investments or a tax credit for home employment or childcare, you have certainly gotten into the habit of cashing out this transfer from the General Directorate of Public Finances (DGFiP) in mid-January. Average amount of the temporary gift from the Public Treasury: 624 euros, the equivalent of 60% of the usual amount of tax credits and reductions of the taxpayers concerned.

| Credits and tax reductions | Average amount of annual benefit * | Average advance amount ** | Number of beneficiaries |

|---|---|---|---|

| Donations to works (tax reduction) | 384 | 132 | 3.3 million |

| Donations to people in difficulty (tax reduction) | 236 | 1.9 million | |

| Union dues (tax credit) | 113 | 54 | 1.3 million |

| Home employment (tax credit) | 1201 | 633 | 4.5 million |

| Childcare costs (tax credit) | 683 | 370 | 1.9 million |

| Hospitality expenses in nursing homes (tax reduction) | 1178 (costs related to dependency) | 391 | 230000 |

| Rental investment (tax reduction) | 4012 (Pinel reduction) | 2380 | 310000 |

Total advance, all devices combined | 624 | 9million | |

* Average credits and reductions paid in 2022, for expenses made in 2021.

** 2019 averages except for the total amount (2023 average)

Source: DGFiP

This advance was created by the State to prevent households from having to advance money to the tax authorities themselves. Because credits and reductions are not yet taken into account in the calculation of the withholding rate at source.

What is the point of modifying or waiving the tax advance?

Problem: Sometimes the lead is overestimated. The proof: approximately 10 million households pay a balance of income tax every year at the end of September. This balance is due to income which has skyrocketed… or an excessively large advance received in January. Which the DGFiP then requests reimbursement. In some cases, the pleasant surprise of January turns into a grimace in September…

How can we explain that the advance is overvalued? It’s a question of timing. The tax authorities calculate this gift on the basis of the last income declaration (in spring 2023, which relates to 2022 income) and the advance concerns the income of the current year (so your salaries or other income for 2023) : hence a calculation that sometimes sticks little with reality. This is why the DGFiP encourages you to modify (or even renounce) your advance.

Who is affected by the correction of the tax advance?

All taxpayers who must receive an advance in January can waive it, via their personal space. L’advance pour into January 2024 will be calculated on the basis of your credits and reductions received in 2023, therefore on the basis of your 2023 declaration relating to the income 2022. However, sometimes the situation has changed… If you are entitled to tax advantages in 2023 but this will no longer be the case in 2024, you will have to repay the advance in September 2024!

Example. You declared childcare costs of 2000 euros for 2022, which entitled you to 1000 euros of tax credit in 2023. The tax authorities will pay you 600 euros in advance in January 2024. Except that your child was 3 years old in 2022 and that you have not paid any childcare costs in 2023. In this case the DGFiP will advance you 600 euros in January 2024… which you will most likely have to return in September.

More than 220,000 tax households have thus lowered the advance which was intended for them last year: very precisely 54,407 requests for a reduction and 155,119 waivers of the DGFiP transfer in mid-January.

The case of the precursors of the immediate home employment advance

Are you one of the hundreds of thousands of households who already use the immediate tax credit advance? You are the first to receive this tax credit each month and therefore more with a one-year delay. Good news, you don’t have to do anything! If you have used (…) the service offered by Urssaf allowing you to benefit from the immediate advance for personal services, the amount of immediate credit received this year will be automatically deducted from the amount of the advance which will be paid to you next January, without any action on your part, announces the DGFiP in the email it sent last year to the households affected by the January advance.

Tax credit: Cesu or service provider, here are instructions for using the immediate advance

How can I request the cancellation or reduction of the advance?

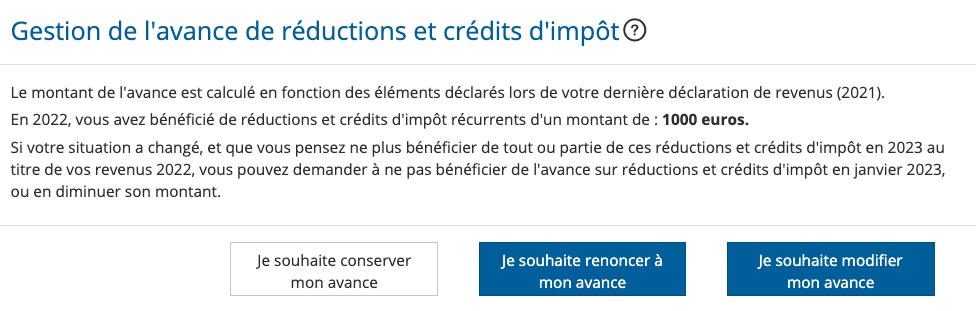

In your space manage my direct debit at sourceon the tax website, click on the button manage your advance tax reductions and credits. The DGFiP reminds you of the total amount of your credits and tax reductions (in 2023 based on 2022 income). Three choices are available to you: preserve in advance, give up or the to modify.

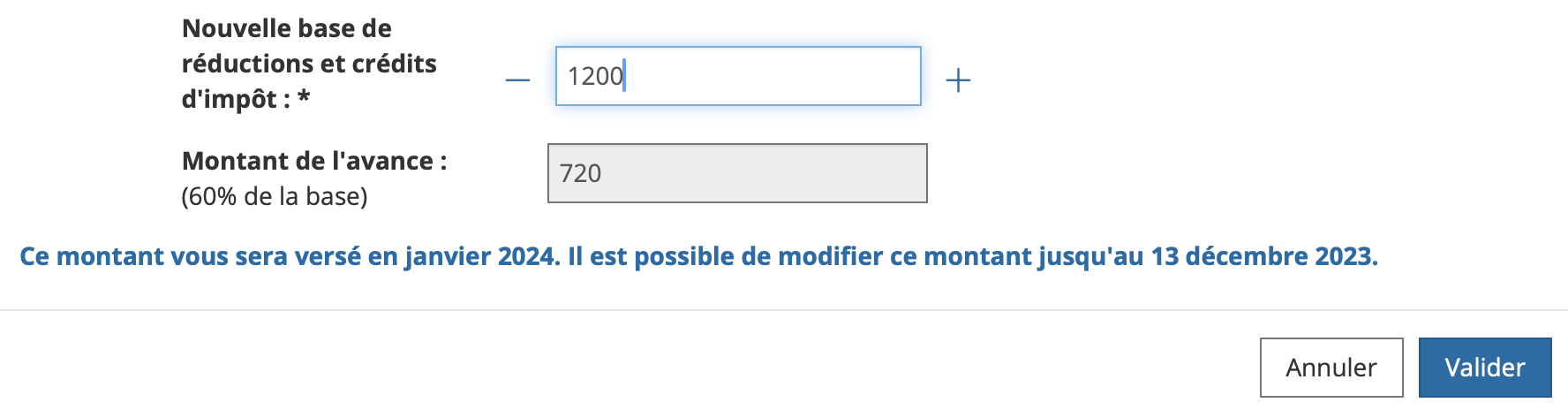

If you choose to modify your advance, the tax authorities then invite you to estimate the total amount of your 2023 tax benefit on the basis of your 2022 income and expenses, using the tax simulator. It’s up to you to fill in the estimated amount, and the DGFiP tells you the recalculated advance. The tax administration specifies in this window that the modulation of the advance is thus open until Wednesday December 13.

You would like inflate the amount that the tax authorities will pay you in January? Too bad… This service does not allow you to increase the amount of the advance, if you believe that your tax advantages will increase.

Please note: if you give up your advance… then change your mind by Wednesday December 13, the tax administration says that you will be able to change your choice until the deadline.

Furthermore, this approach of removing or modifying the advance is completely optional: you can therefore consciously choose to keep this excess capital advance in January. Just have enough money to pay it back in September 2024!

Taxes, property tax and housing tax: dates anticipated in December