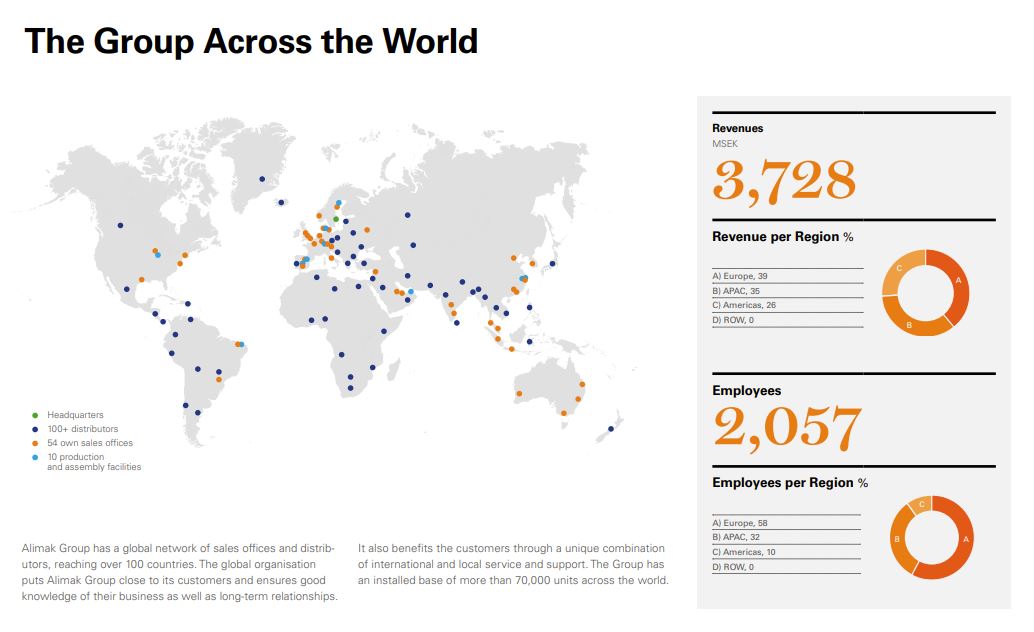

It naturally has a large exposure to the construction and industry sector (80% of turnover between them), with however a promising development of the wind activity even if it still remains thin in the mix (10 % of sales).

The turnover is well broken down geographically with 10% in Australia, 10% in China, 20% in the United States, 35% in Europe, 15% in the Middle East and 10% in the rest of the world. Gaining market share in North America is a priority for the group. We will appreciate the lesser concentration on China where there has been a real boom in the construction of skyscrapers over the past three decades. However, this cycle seems to have come to an end. Alimak will therefore not suffer too much from the slowdown in construction in China.

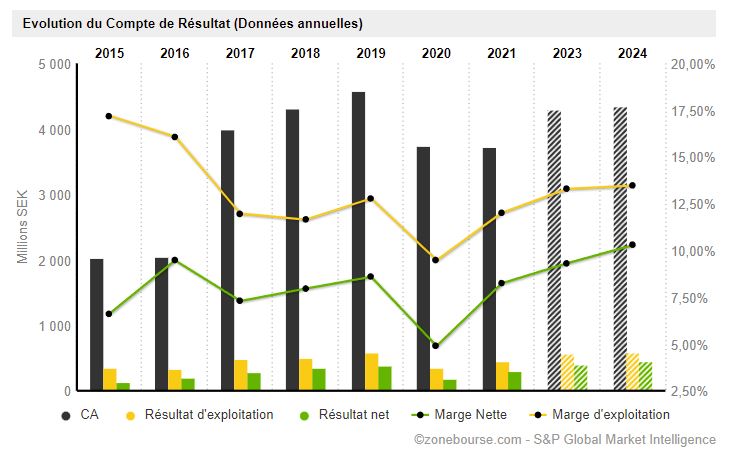

Due to a significant change in scope in 2017, linked to the acquisition of Facade Access Group, we will mainly analyze the operational path over the last five years (2017-2022). Over this period, cumulatively, Alimak generated $180 million in book profits and $230 million in cash profits (the famous “free cash-flows” that we love so much at Zonebourse). The difference of $50 million between the two is mainly due to a sharp decrease in WCR (working capital requirement) with the liquidation of inventories during the pandemic.

At constant scope, all things being equal and based on accounting profits, we are on an annual earning capacity of 36 million dollars. As there is not really any organic growth or acquisitions, we will start on this base of 36 million dollars.

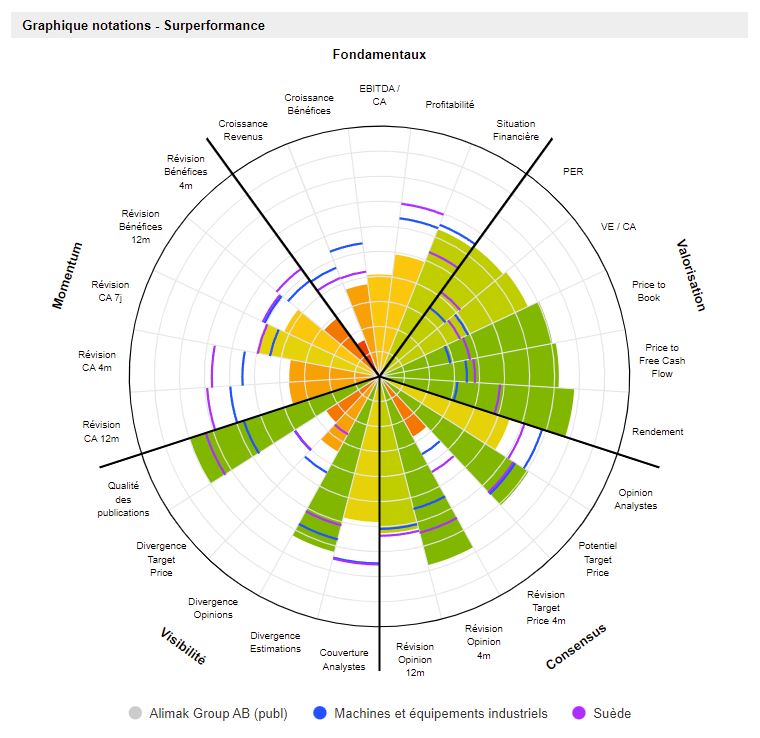

At the current price of 80 SEK – this is to be compared to a market capitalization of 4.2 billion SEK or 400 million dollars – the value is paid approximately 11 times the profits, or almost two times less than the average valuation of the five last years. A good point, especially since the fundamentals have not deteriorated since then, quite the contrary. At this level of valuation, there is not yet a considerable “safety margin”, a concept dear to Benjamin Graham or Seth Klarman, but it is starting to become interesting for investors who are rather risk averse. We are indeed in a fearful market faced with the potential risk of recession. To reassure ourselves, we can mention that the P/E level is valued on these ten-year lows.

Another advantage of the situation, beyond the correct fundamentals and the attractive valuation, is the presence in the capital of the very reputable investment holding Latour AB which holds 30% of the shares and will undoubtedly support the external growth strategy. as they are used to doing well with their other participations. It’s a real asset to have such a supporting reference shareholder, both to weather the storm and to ensure expansion and favorable financing conditions.

Moreover, we can note that the exchange rate is currently rather favorable to the EUR/SEK which facilitates the entry of investors in euros on the Swedish market. The Swedish krona is also a famous currency (see: video by Xavier Delmas on the EUR/USD parity). This configuration is a priori rather stable because the Swedish economy is very dependent on exports to the euro zone. Their currency must therefore be attractive to buyers in euros.

In the meantime, the group is paying a 5% dividend well covered by cash flows, which is always worth taking, especially at this time.

The insiders buy at the market (and they started to do so at higher prices than the current one). This is always a significant sign in these troubled times: management finds the action undervalued.

To conclude, we are dealing with a profitable company whose balance sheet is healthy, without excessive debt or potential solvency problems. The growth is certainly not impressive, but the activity is surprisingly not very capital intensive even if the return on equity remains all in all modest at around 10%. It remains a small-cap, therefore reserved for investors who are a little more seasoned and able to regularly monitor the company.