When you take out a consumer loan, the lending institution often wants to insure you. However, in certain cases, this loan insurance only covers you very little.

2000 euros to buy household appliances, 6000 euros to redo your kitchen or even 12,000 euros to be able to buy a used car… Consumer credit allows many borrowers to carry out a project or face an unexpected expense. When taking out a loan, the borrower will be asked, more or less insistently, to take out loan insurance.

Consumer credit: how banks put pressure on you to take out borrower insurance

Credit insurance is intended to protect the borrower, recalls in the preamble Jean-Louis Kiehl, president of Crsus, an association which fights against over-indebtedness. Several options are then available. All organizations offer DIM (Dcs, Disability, Sickness) insurance. This coverage includes three guarantees: death, total and irreversible loss of autonomy (PTIA) and total temporary incapacity for work (ITT). It ensures the payment, under certain conditions, of the remaining capital due in the event of the death of the insured, or monthly payments if the insured person is completely off work for medical reasons.

It is also possible in certain cases to take out DIMC insurance (Death, Disability, Sickness, Unemployment), which also insures you, on paper, in the event of job loss. If lending institutions do everything to insure the borrower, let us first remember that, if it is almost obligatory when taking out a real estate loan, Insurance remains optional in the context of consumer credit.

90 days franchise on average for the ITT guarantee

But even by taking out insurance, the borrower is exposed to unpleasant surprises. Because there are numerous clauses and exclusions surrounding consumer credit insurance. The majority of the establishments tested (Cofidis, Sofinco, Cetelem, Floa Bank, Franfinance and Younited Credit) report a 90-day exemption before compensation in the event of total temporary interruption of work (ITT), during which the borrower must continue paying your credit.

However, according to the 2023 work stoppage observatory, produced by the Apicil group, the average duration of work stoppages in 2022 was 22.13 days. However, the ITT guarantee is put in place for long-term shutdowns (more than 6 months), says Mal Bernier, communications director at Meilleurtaux. If you are off work for 15 days or three weeks, you will not have any loss of salary, that is why there is a deficiency. The guarantee is there to take over.

The problem is that even in the event of long-term interruption, borrower insurance excludes many pathologies, and it is not easy to navigate because of the insurance notices provided by the lending institutions. often lack clarity.

In its 2022 report, the insurance mediator also indicated that it had noted vague exclusion clauses condemned for a long time by the Court of Cassation. In personal insurance, these are mental disorders or any other back painnotions that the Court of Cassation considered vague and therefore contrary to the law, and which requires that these clauses be precise, formal and limited.

An opinion shared by Jean-Louis Kiehl, who denounces a problem of readability of insurance contracts. According to him, if insurance provides a guarantee for the consumer, we must do better with information, by providing the data in a much clearer manner, without drowning it in an insurance notice. There is a need for clarity, because the citizen is not a professional insurer, he is not aware of the subtleties of the clauses and exclusions.

Many pathologies excluded

One thing is certain, back problems are very often excluded from guarantees in the insurance notices consulted by MoneyVox. However, these concerns, classified in the category of musculoskeletal disorders (MSD), are the second factor in work stoppages in cases longer than 30 days according to the 2023 Work Stoppage Observatory published by the Apicil group: 29% among those under 30, 35% among those over 30.

Thus, Cetelem explains that the compensation conditions apply to any accident or illness occurring after the effective date of the guarantees, exclusion of the following cases: disco-vertebral injuries and their consequences not requiring surgical intervention within 3 months following the first day of sick leave.

For its part, Floa Bank excludes from its guarantees disc or vertebral damage: lumbago, low back pain, sciatica, back pain, neck pain, cervico-brachial neuralgia, disc herniation, unless these conditions require surgical intervention with hospitalization for more than 30 days continuous (excluding day hospitalization at home).

Cofidis, however, agrees to cover these illnesses, as long as they have not occurred and been known to the insured on the day the membership application is signed. For its part, Sofinco compensates disabilities of back-lumbar origin within the limit of 6 monthly payments (except surgical treatment).

Coverage is not better for psychological pathologies, while between 2020 and 2022, they have become the leading cause of work stoppage for periods of more than 30 days, according to the Apicil group. They represent 35% of arrests followed among those under 30, and almost 40% among those over 30.

For these pathologies, Cofidis explains that Depressive states are excluded, whatever their nature., when Cetelem talks about his side of exclusion for anxiety-depressive disorders. Franfinance and Sofinco expressly exclude burn-out and chronic fatigue. And even the illnesses covered are only covered for a period: For each of the guarantees Temporary Total Incapacity for work and Loss of Job following dismissal, the coverage cannot exceed 18 monthly reimbursements in one or more claims, let Cetelem know, for example, when Cofidis stops at 15 monthly payments.

Concerning the death guarantee, it is also better to look at the small details of the contract. The consequences of the use of narcotics, hallucinogens or medications not prescribed medically or used in doses not respecting the medical prescription, suicides occurring during the first year of the contract or even the state of intoxication when the insured was driving the accident vehicle and the conditions resulting from the state of chronic alcoholism.

Restrictions may also be put in place depending on the age of the borrower. The death guarantee is thus offered until the borrower’s 78th birthday at Cofidis, 80 years at Cofidis and 83 years at Sofinco.

A job loss guarantee not always useful

Finally, if you take out loss of employment insurance (valid only in the event of dismissal without serious misconduct), you must first see a waiting period of 180 days pass, i.e. almost 6 months before this guarantee is active. And in some cases, this period is accompanied by an additional 90 days of exemption. That is 9 months between taking out the insurance and taking out the credit.

The job loss guarantee covers quite poorly in France, confirms Mal Bernier. In the majority of cases, borrowers can do without it. But this is not always obvious. Floa Bank, for example, only offers two choices: take the DIMC package or not take out insurance.

If on a small loan repaid quickly, it is not useful, you have to think about it when you take out a long loan which represents tens of thousands of euros

Faced with all these elements, should we then take out borrower insurance? Everything ultimately depends on the duration and amount of the loan: If on a small loan repaid quickly, it is not useful, you have to think about it when you take out a long loan which represents tens of thousands of euros, because the insurance remains a protection for the borrower and his loved ones , judge Mal Bernier.

Because as the legal notice says, a credit binds you and must be repaid. If the borrower is unable to do so, the lending institution can turn to his heirs (in the event of death) or force him to repay even if he is in difficulty. If you think you will have difficulty repaying your credit in the event of a life accident, thinking about taking out insurance for your loan is not a bad idea.

It is not perfect insurance, it is much worse than real estate credit insurance, concludes Mal Bernier. It’s only for 2000 or 5000 euros, it’s not necessarily worth taking. But from 15,000 euros or for a loan beyond 36 monthsI find that the question really arises.

The problem of non-use of subscribed insurance

But you still have to think about it when using it. There is a problem of citizens not taking up insurance, confirms Jean-Louis Kiehl. They take out insurance that could protect them in the event of disability, yet implementation is quite weak, because people forget that they have taken out this insurance. It’s a box they check, sometimes almost without realizing it, and they forget it. For the president of Crsus, policyholders must therefore take the time to read the contracts they subscribe to.

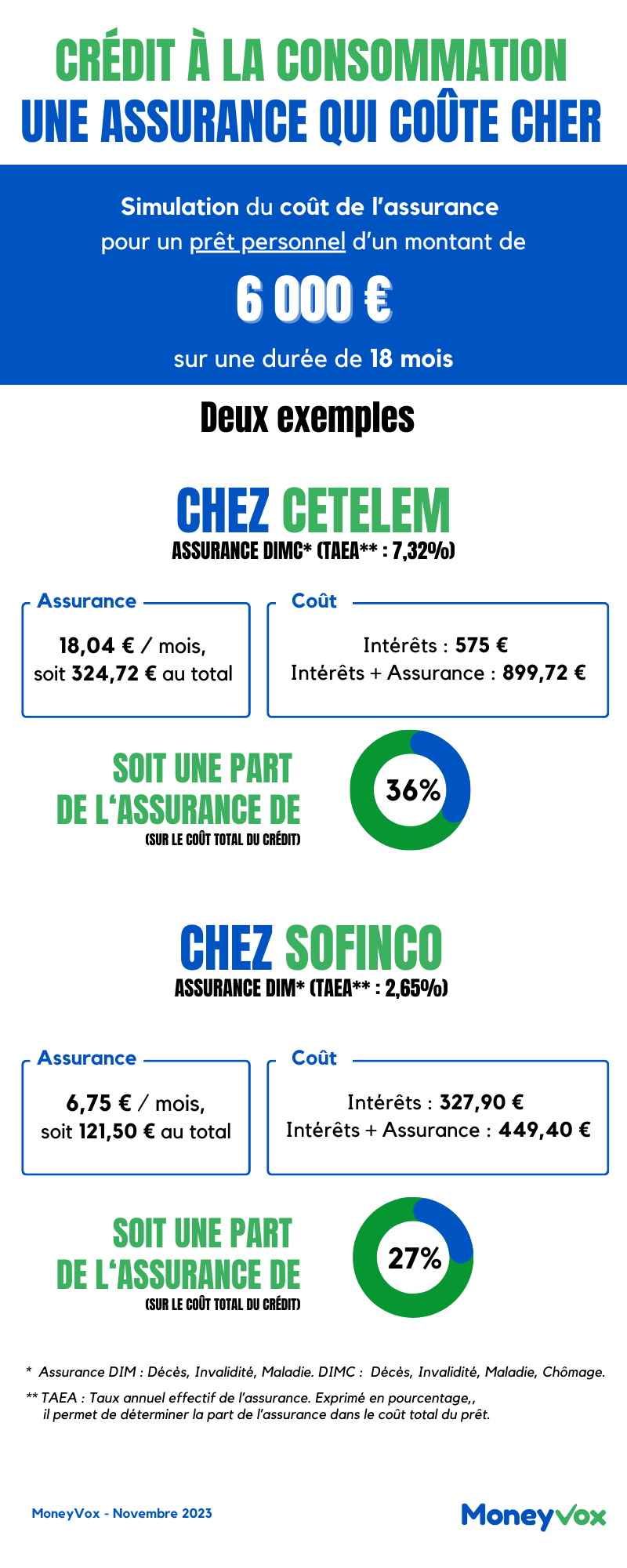

Consumer credit: the lucrative business of borrower insurance which is very expensive for consumers

While waiting for the insurers themselves to take matters into their own hands? There is a movement taking place, on the side of insurers, like Axa or Cardiff who are starting consider insurance that would simplify the information for use by policyholders. This would make insurance more transparent, judge Jean-Louis Kiehl. And other simple solutions could be put in place. The insurer could for example, every year, remind the insured by a message that he or she is covered.