|

|

| Tops / Flops of the week |

Fortum (+27%): Germany’s decision to take control of Uniper, Fortum’s subsidiary, has taken a major thorn out of its future ex-Finnish parent company. The operation certainly took place at a low price, but to adopt a slightly violent image, the investors prefer the amputation to the gangrene of the whole group.

CanoHealth (+25%): Nothing like speculation to escape a week of slump in the markets. Humana and CVS Health are said to be in the running to buy the retirement home operator. Cano has been under pressure for months by the activist fund Third Point (6.4% stake), which wants the company to be bought.

OVS (+17%): The Italian clothing brand published good results for the second quarter. Analysts praise the quality of the economic model, which allows prices to be increased without putting too much strain on demand.

Rheinmetall (+11%): The return of the Ukrainian conflict to the forefront of the media scene with the conscription of Russian reservists announced by Vladimir Putin has caused a renewed appetite among investors for defense stocks. A visible attraction also on BAE Systems, Leonardo or Thales this week.

General Mills (+7%): The American agri-food group, known in particular through its brands Cheerios, Häagen-Dazs, Old El Paso or Yoplait, raised its annual forecasts this week for the financial year which will end at the end of next May.

Advanced Micro Devices (-9%): Technology stocks had a difficult week. The semiconductor compartment even more. AMD is down more than 50% since the start of the year.

Uber (-11%): The group was the victim of a cyberattack at the end of last week. The company accuses a hacker affiliated with the Lapsus$ group. The attack forced Uber to shut down some internal systems. At this stage, the damage has not been specifically made public.

Ford-Motor (-13%): The manufacturer warned about its Q3 results. It said rising supplier costs (about $1 billion more than expected) are expected to affect its quarterly profits, while shortages prevent it from completing some already-assembled vehicles.

Swiss credit (-13%): The Swiss bank is still in the eye of the storm. New rumors are circulating about the future strategy, after the failures accumulated in recent years. Capital increase, departure from the United States, split within the investment bank… All these noises from the corridors weigh on the course of the action.

|

| Raw materials |

Energy : The monetary tightening by the Fed, but also by other central banks, weighs on the compartment of risky assets, such as oil. Operators continue to see the glass half empty, concerned about the consequences on demand of monetary tightening, which can be described as generalized. In this context, the new rise in tensions in Ukraine, where the Kremlin has planned referendums to annex 4 Ukrainian regions as well as the mobilization of 300,000 reservists, takes a back seat. The EU is reportedly considering new sanctions against Moscow, including a price cap on Russian oil. Nevertheless, reaching a consensus could prove difficult due to the position of certain countries such as Hungary. North Sea Brent is trading around USD 85 while US WTI is trading at a discount of almost USD 7 to USD 78 per barrel.

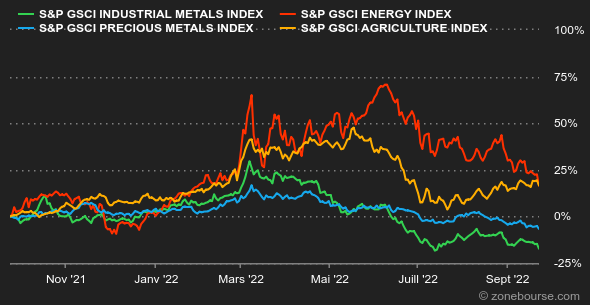

Metals : The strengthening of the dollar weighed on the compartment of industrial metals, with the exception of nickel and tin which stabilized at 24560 and 21650 USD respectively. Rio Tinto’s forecasts also weighed on market sentiment as the mining group predicts a “difficult” environment for copper in the short term due to soaring prices, which could weigh on demand for the metals. Finally, zinc inventories recorded a further decline within the LME facilities to reach their lowest level since February 2020. On the precious metals side, gold is resisting a bit and is stabilizing around USD 1670.

Agricultural products : Rising friction in Ukraine has supported wheat prices as it raises new concerns about compliance with Black Sea supply agreements. Wheat is trading near 900 cents a bushel in Chicago, versus 680 cents for corn. |

|

| Macroeconomics |

Vibe : Everyone got it right this time? The US central bank has reiterated, but raised its tone, that the fight against inflation will be tough, complicated and long. Other countries have also tightened the screw, from Norway to Switzerland via the United Kingdom. The impact of these restrictive monetary policies can already be seen on the activity indices, but not yet really on prices… hence some distress among investors.

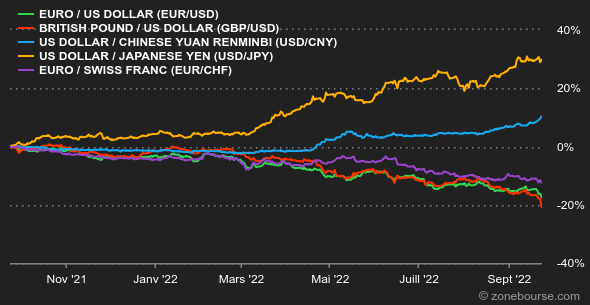

Currencies : Two important news this week. On the one hand, the euro is testing lows against the dollar, below the bar of 0.98 USD for 1 EUR. On the other hand, the Bank of Japan wants to signal the end of the yen’s slide against the greenback (-25% since 1er January). It intervened in the market for the first time in the millennium to protect the bar of 145 JPY for 1 USD. Currency traders are not really surprised, but are wondering how the BoJ can withstand the shock while continuing its accommodative policy.

Rate : The determination of the Fed has caused the last levees to break in the bond market. The yield on US 10-year debt rose from 3.47% last week to 3.77% on Friday. The yield curve is still inverted with the 2-year maturity, yielding 4.24%. In Europe, the trajectory is identical with more marked increases among issuers deemed less qualitative. The Swiss debt is at 1.37% over 10 years, the German Bund at 2.04%, the French OAT at 2.62% and the Italian BTP at 4.31%. The British Gilt reached 3.76%.

Cryptocurrencies : Cryptocurrencies remain under pressure like the rest of financial assets. Bitcoin is below 19,000 USD per unit (-9% over one month) while Ether is trading around 1290 USD (-18% over one month).

|

|

|

| Items of the week | ||||||

|

| *The weekly variations of the indices and stocks displayed on the dashboard relate to the period from Monday when the respective markets open to Friday when this newsletter is sent. The weekly variations of raw materials, precious metals and currencies displayed on the dashboard relate to a period over 7 rolling days from Friday to Friday until the sending of this newsletter. These assets continue to trade on weekends. |

Zonebourse.com 2022