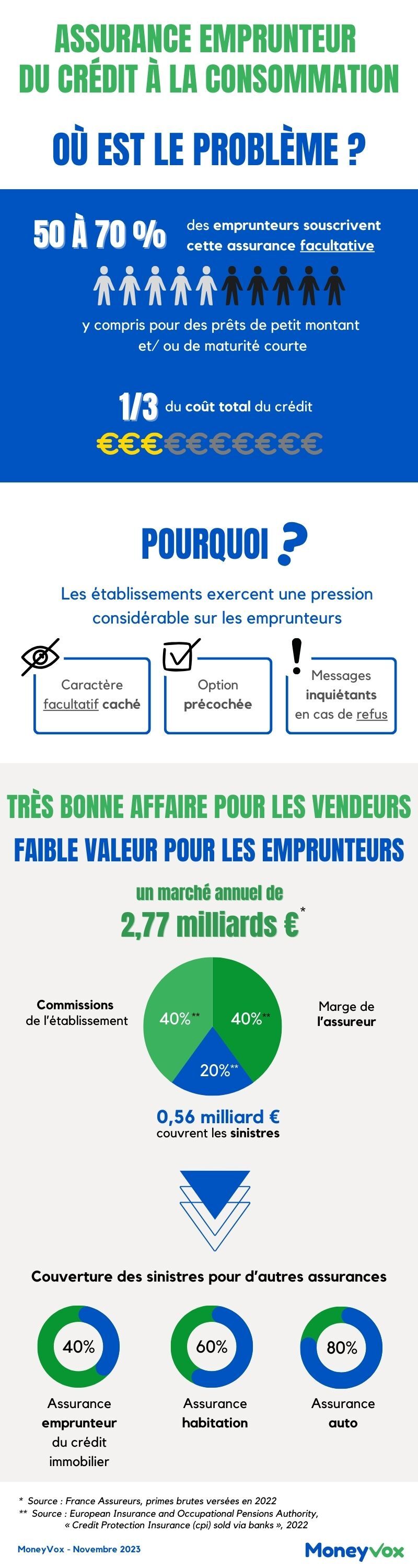

It is optional. However, when you take out a consumer loan, credit institutions strongly encourage you to take out borrower insurance, regardless of the amount borrowed and the repayment period. At the cost, sometimes, of a certain opacity. We have testing for you.

The question does not arise when you take out a real estate loan. For a consumer loan, on the other hand, you have the choice: that of insuring yourself, or not, against alas (death, disability, illness or unemployment) which could prevent you from repaying your debt.

In terms of consumer credit, in fact, borrower insurance is optional. She is no less systematically offered by credit institutions, face-to-face as in the online subscription process. Often with insistence and a certain opacity, as we have seen.

We have carried out loan simulations on the websites of six major players in the personal market (in parentheses, the names of the insurers with which they work):

- Cetelem (BNP Paribas Cardiff)

- Cofidis (ACM)

- FLOA (ACM Vie, Serenis Assurances)

- Franfinance (Sogecap, Sogessur)

- Sofinco (CACI Life and Non-Life, Fidelia)

- Younited Credit (MetLife Europe)

The findings vary depending on the brand. Transparency efforts exist among some (Cetelem, Franfinance, Sofinco), less so among others (Cofidis, FLOA, Younited). All, on the other hand, have one thing in common: whatever the profile used (husband or not, private sector employee or civil servant, owner or tenant, average or comfortable income), the amount requested and the repayment period chosen, borrower insurance is systematically recommended. Including for loans of average amount (4000 euros) and short repayment period (12 months).

Insurance (more or less) discreetly optional

As with a real estate loan, a bank can perfectly choose to make the granting of a consumer loan conditional on the subscription of insurance guaranteeing its reimbursement. In fact, this is never the case: borrower insurance is optional in all establishments the granting of which we have tested.

For a simple reason: if insurance is compulsory, its cost must be considered in the calculation of the APR (total annual effective rate), itself limited by the wear thresholds, the maximum rates authorized by the regulations. This reduces the margin available to institutions to make their loans profitable.

This optional character, however, is not not always highlighted. Without ambiguity at Cetelem or Franfinance, the mention of optional insurance is present in a more discreet manner in the proposals of Cofidis, FLOA, Sofinco or even Younited.

An option sometimes unchecked

A sign of the importance it has for credit organizations, insurance is systematically highlighted in the subscription process. Indispensable security in the event of life’s hazards, indicates Cofidis. Taking out a loan is an important project! We advise you to take out our insurance offer, displays Younited Credit.

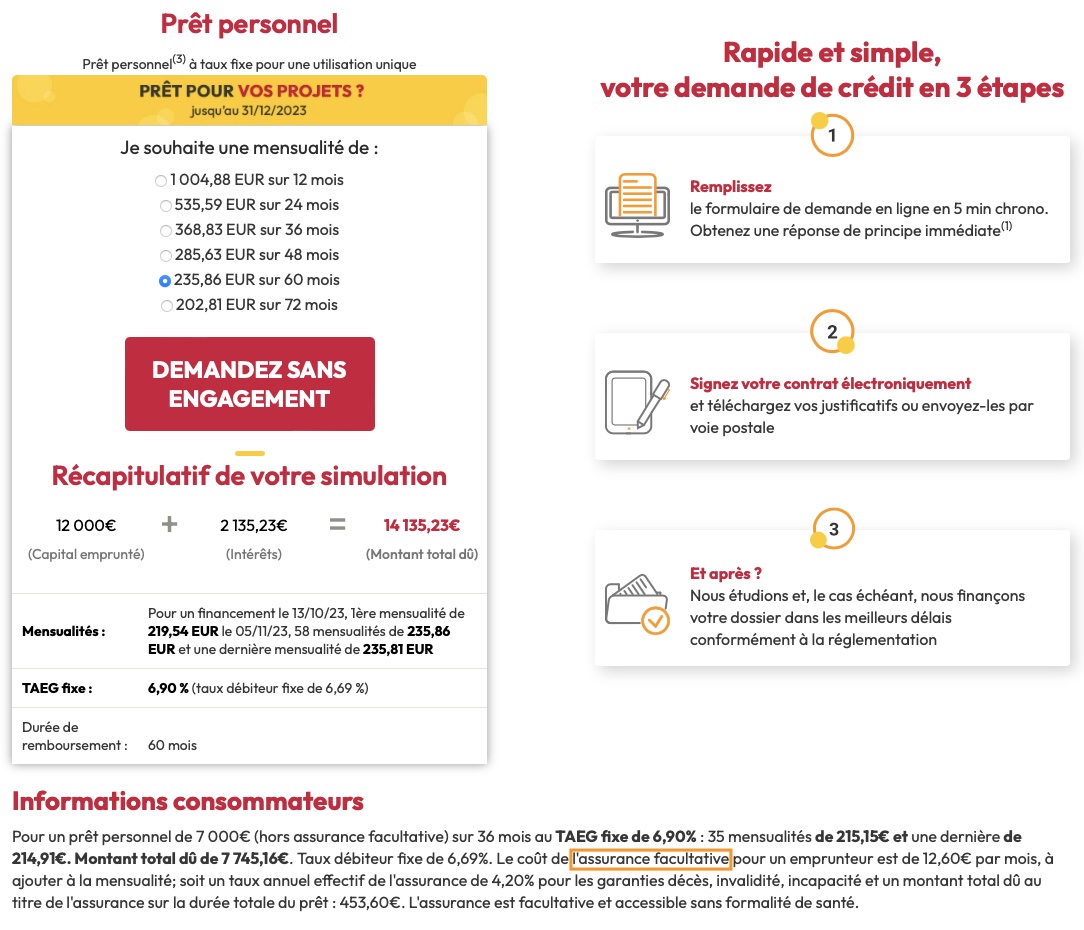

Messages of encouragement that appear whatever the project, for a car loan of 12,000 euros over 5 years as for a cash loan of 4,000 euros over 12 months. However, in the second case, the interest in insuring yourself is much more questionable…

Exclusions, waiting periods… Is it in your interest to take out insurance for a consumer loan?

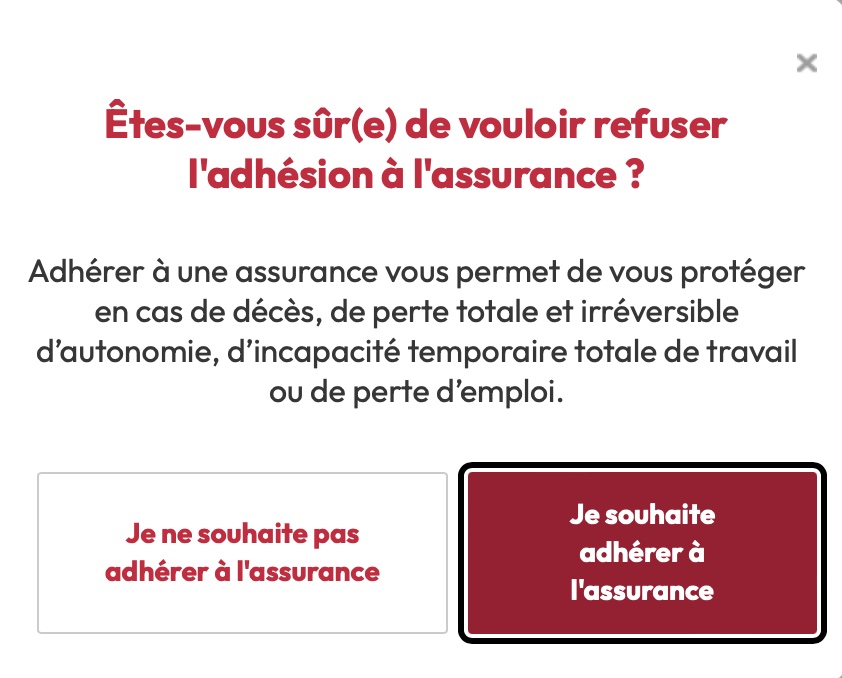

The eagerness of certain credit institutions to sell insurance is also evident in the how to obtain your consent. Two actors, FLOA and Younited, practice what is called a passive opt-in: the insurance option is active by default. If the borrower wishes to do without it, he must uncheck before validating this step. A practice that is surprising in the case of a product that is supposed to be optional.

FLOA is the only establishment that agreed to answer our questions orally. Marc Lanvin, its deputy general director, told us that this is a project on which [FLOA] is committed to providing increased transparency.

Worrying messages

Have you chosen to do without insurance? Please note: in this case all test organisms display a warning message with, often, the possibility of going back with a simple click. In the case of Sofinco, you must confirm your refusal of insurance twice. A procedure, obviously, likely to worry the borrower who has chosen to do without it.

Advice reduced to its simplest expression

If credit institutions act as intermediaries between the borrower and the insurance company, they are not exempt from obligations. Here is the framework set by the Insurance Code (1): distributors of insurance products act in an honest, impartial and professional manner, in the best interests of the subscriber or member. They must advise a contract which is consistent with the requirements and needs of the potential subscriber or prospective member and specifies the reasons for this advice.

According to our experience, no establishment really adapts the advice the type of loan requested and the profile of the borrower. We were not able to test all possible configurations. But we varied the amounts (12,000, 6,000, 4,000, 2,000 euros), the reasons for borrowing (purchase of a car, fitting out a kitchen, cash flow needs), the profiles of borrowers (single, married couple, civil servant, executive). private, etc.). For the same result: the recommended insurance was systematically the most comprehensive possible, and therefore the most expensive.

Loss of employment sometimes offers civil servants

With one nuance, concerning the job loss guarantee, which covers the borrower who loses his job and finds himself unemployed (on condition of being compensated by Ple Emploi). Faced with the request of a civil servant who, by definition, is protected from unemployment, 2 of the 6 organizations tested (Cetelem, Franfinance) do not advise him to take out job loss guarantee. This coverage, moreover, is absent at Sofinco and systematically optional at Younited.

At Cofidis and FLOA on the other hand, the job loss guarantee is offered every time, including to civil servants. Worse, at FLOA, it is impossible to adjust guarantees: either you insure yourself for everything (death, disability, illness, loss of job), or you do not insure yourself. A choice made by Marc Lanvin: We are obsessed with making our subscription process as simple as possible. Offering a single insurance for all borrower profiles is the choice of pooling and security.

To clarify his choice, the consumer can, in theory, refer pre-contractual information that establishments have the obligation to make available to the future borrower and policyholder. You still have to find it (its provision is sometimes discreet) and succeed in reading it. Some establishments, in fact, bring together all the regulatory forms (credit + insurance) in the same document. Result: the latter sometimes reaches 17 pages!

Only advantages for the lender

This is obviously not a question of denying the benefit of borrower insurance for consumer loans. If the stakes are obviously lower than for a real estate loan, due to lower borrowing amounts and shorter repayment periods, ensuring repayment of your consumer loan provides security.

Especially since consumer credit is by definition aimed at people who do not have the means to otherwise finance the purchase of a consumer good, notes David Echevin, CEO of Actelior, an actuarial consulting company. . Among them, we find people who may be more exposed than others to the consequences of a life accident.

However, Do all consumer credits deserve to be insured?, whatever the loan amount, the repayment period and the borrower’s profile? Is the value of this product the same for all borrowers? For credit institutions, in any case, it is certain: borrower insurance only has advantages. It allows them to secure the repayment of the loans they grant, while earning income since they are commissioned by insurers.

Consumer credit: the lucrative business of borrower insurance which is very expensive for consumers

(1) In particular in articles L521-1 and L 521-4 of the insurance code