With the rise in interest rates, the borrowing capacity of households is melting like snow in the sun, by around 20% over two years. But then, how much is it possible to borrow now with current rates? Here are three simulations.

Have you become owners over the last three years and you think you might as well have become owners today? With the rise in real estate rates and the growing reluctance of banks, nothing is less certain, as the real estate credit market is changing rapidly.

In May 2021, the average rate over 20 years was 1.10%, when it is trading today at 3.40% according to the broker Meilleurtaux, more than triple. Faced with this phenomenon, obtaining credit becomes more and more complicated. Difficult for example today to convince the bank without an increasingly high personal contribution. As proof, according to Meilleurtaux, 50-60 year olds brought 54,590 euros in 2019, against 87,209 euros in 2022. But then, how much is it possible to borrow today according to one’s income? MoneyVox offers three simulations to see more clearly.

Take the example of Pierre, a young man wishing to take out a loan for a first real estate purchase. With a salary of 2000 euros net per month, the first-time buyer can claim monthly payments of 700 euros, or 35% debt ratio, according to the standards imposed by the High Council for Financial Stability (HCSF). Aged 27, Pierre can easily claim a 25-year loan, the longest term, at a rate of 3.60%. With all these elements, and provided that his file does not show any default, Pierre can hope to borrow 136,000 euros in June 2023. Two years earlier, in May 2021, the average rate was 1.35%. at the time, with the same criteria, Pierre could have borrowed a little more than 174,000 euros.

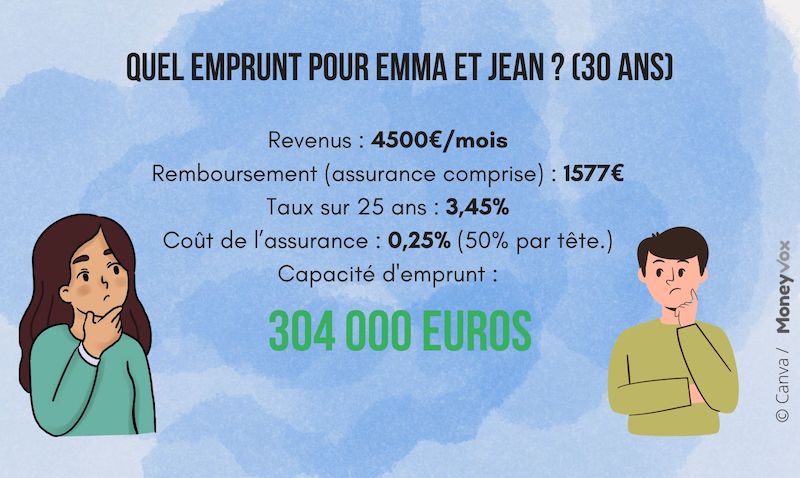

Another example is that of a couple in their thirties, also seeking to acquire their main residence. two, the couple has a net income of 4500euros per month. With the 35% rule, Emma and John can invest up to 1577euros per month in their mortgage. With these monthly payments and a 25-year loan at a rate of 3.45%, the couple can now borrow 304,000 euros. Two years ago, the couple could have benefited from a rate of 1.3% over 25 years. His envelope would then have been 383,000 euros, not counting the personal contribution. That is a loss of 79,000 euros, the equivalent 20% of its borrowing capacity. Although real estate prices are starting to fall, the fall is still too slight to offset the rise in interest.

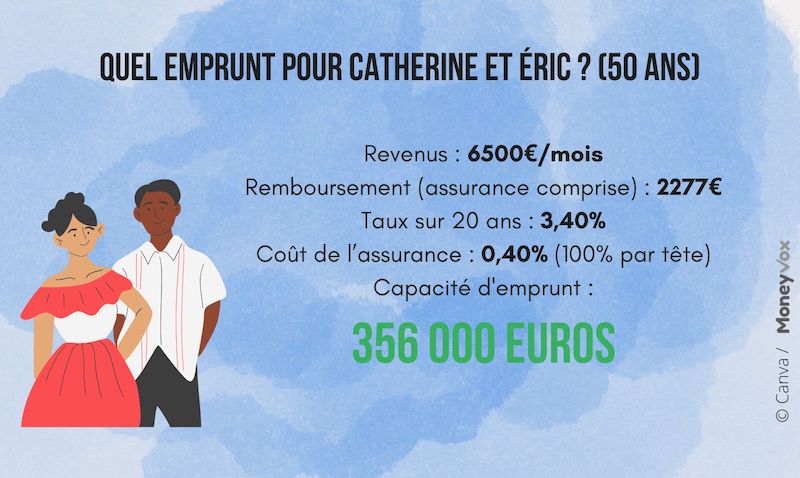

Last example, that of Catherine and ric. With 6,500 euros net per month, the couple can claim monthly payments of 2,277 euros. Nevertheless, aged about fifty years, the bank prefers to offer them a loan over 20 years, at a rate of 3.40%. Under these conditions, their borrowing capacity is therefore 356,000 euros in June 2023, against nearly 429,000 euros two years earlier, again without counting the contribution, i.e. a drop of just over 20% in their borrowing capacity.

The French who can still borrow therefore see their real estate purchasing power inexorably amputated. And many households can no longer even borrow. The tightening of access to credit and the contraction in banking supply are weighing on demand weakened by the loss of purchasing power and the rise in mortgage rates. Access to the market is therefore becoming more and more difficult, details the Crédit Logement/CSA Observatory. In this context, over one year, the number of loans granted was down 35.1% in May 2023, according to the Observatory.

Real estate loan: find the best rate